If you’re looking to get equipment financing, understanding the approval process can save you time and frustration. You might wonder, “What does it take to get approved?” or “How do I know if I qualify?” Knowing the key steps and requirements for an equipment finance approval check puts you in control.

This guide will walk you through what lenders look for, how your credit score affects your chances, and what documents you’ll need ready. By the end, you’ll feel confident about navigating the approval process and securing the financing your business needs.

Keep reading to make sure your equipment finance approval goes smoothly and quickly.

Credit Score Requirements

Minimum credit scores for equipment finance usually start around 600 to 650. Scores above 700 improve chances of approval and better rates. Lenders often check your credit history to see payment habits and debt levels. A clean record shows you are a reliable borrower.

Late payments, defaults, or bankruptcies can hurt your approval. They make lenders cautious. Some lenders may still offer financing but at higher costs.

Improving your credit helps. Pay bills on time and reduce debts. Keep credit card balances low. Check your credit report for mistakes and fix them quickly. A better score can lead to easier approval and lower interest rates.

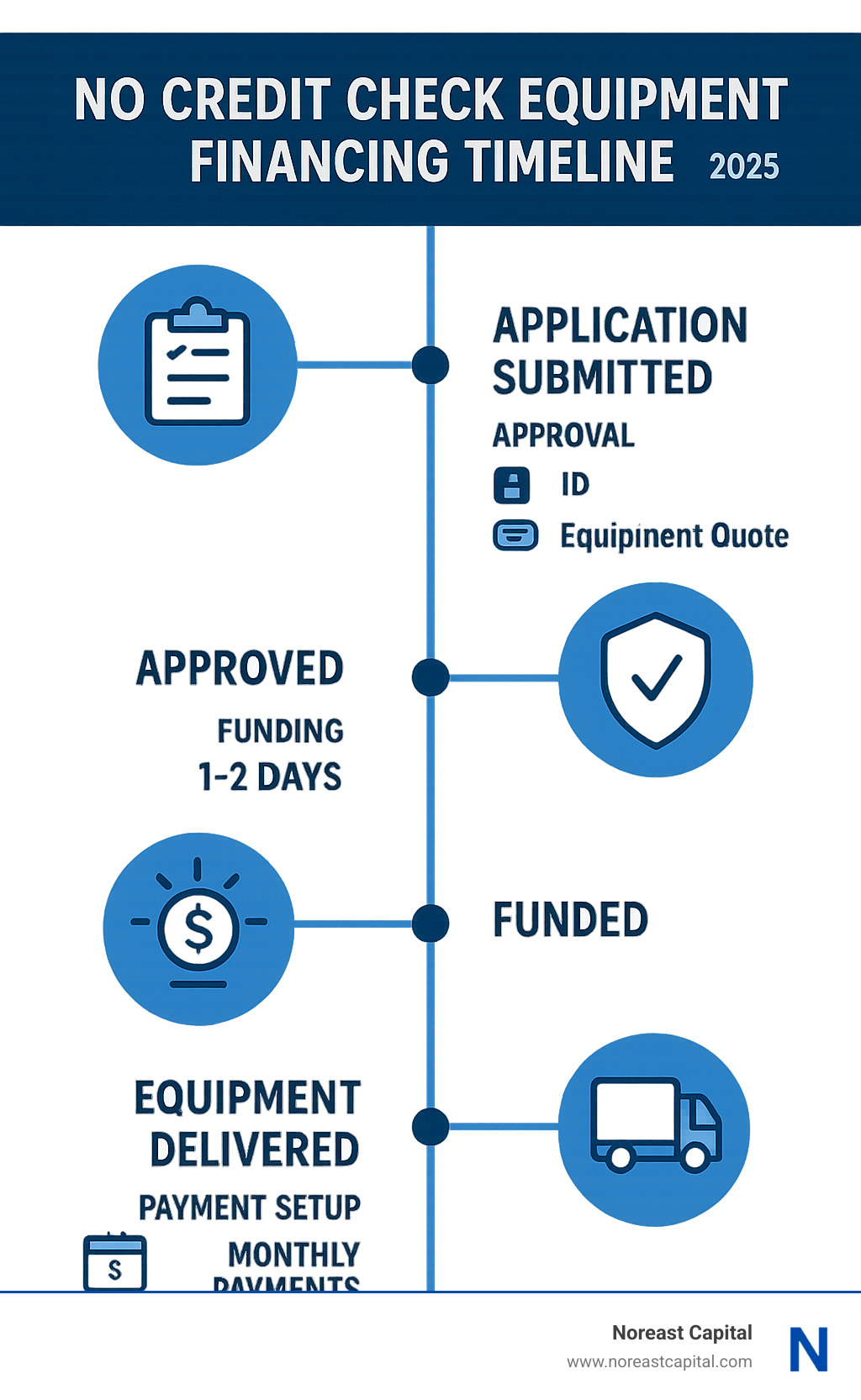

Application Process

Required documents usually include business financial statements, tax returns, and identification. Lenders often ask for proof of income and business licenses. Having these ready speeds up the process.

Steps to apply start with filling out the application form carefully. Submit all required documents. Next, wait for the lender to review your information. They may ask for more details before approval.

Common mistakes to avoid include submitting incomplete forms or missing documents. Avoid overstating your income or assets. Double-check all information for accuracy. These errors can delay or stop approval.

Approval Factors

Financial stability plays a key role in equipment finance approval. Lenders check if your business has steady income and good credit history. They want to see you can repay the loan on time. A strong financial record means higher chances of approval.

Collateral matters a lot too. Many lenders ask for assets like equipment or property as security. This lowers their risk if you fail to pay. The value and condition of the collateral affect the loan terms and amount.

Business revenue is also important. Lenders prefer companies with consistent and sufficient income. This shows your ability to handle monthly payments. They may look at recent tax returns, bank statements, and profit reports to decide.

Speeding Up Approval

Pre-approval can save valuable time in the equipment finance process. It helps show lenders that you are serious and ready to move forward quickly. Having your financial documents ready and knowing your credit score also speeds up approval.

Choosing the right lender matters. Some lenders specialize in certain industries or equipment types. Comparing offers can find better rates and terms. Look for lenders with clear requirements and fast responses.

Online tools make the process easier. Many websites offer pre-approval checks and loan calculators. These tools give quick estimates on what you might qualify for. Using them helps plan your financing before applying.

Options For Low Credit

Alternative financing solutions help businesses with low credit scores get equipment. These options often include lease agreements, vendor financing, and microloans. They do not always require a perfect credit score but may have higher interest rates.

No credit check offers are available from some lenders. These deals focus on business cash flow instead of credit history. Approval is faster, but terms might be stricter or costs higher.

Building credit is key for better loan options in the future. Paying bills on time, reducing debt, and keeping credit use low can improve scores. Over time, this leads to more financing choices and better rates.

Equipment Financing Types

New equipment loans usually have lower interest rates and longer repayment terms. They help businesses get the latest machines with full warranties. Used equipment loans cost less but may have higher rates and shorter terms. This option suits companies with tight budgets or less need for new tech.

Short-term financing lasts less than two years and helps with quick purchases or cash flow needs. It often has higher payments but less total interest. Long-term financing spreads payments over many years, lowering monthly costs. It fits big investments but may cost more overall.

Leasing lets businesses use equipment without owning it. Monthly payments are usually lower, and upgrades are easier. But there is no asset ownership. Buying means full ownership after payments end, adding value to the company. It may require more money upfront or higher monthly costs.

Local Resources In Austin

Austin offers several top lenders nearby who specialize in equipment finance. These lenders provide flexible terms and quick approvals to help local businesses grow. Many have offices in the city, making it easy to get personalized service and support.

Community financial programs in Austin focus on helping small and medium businesses access funds. These programs often offer lower interest rates and grants for qualifying businesses. They work closely with lenders to improve your chance of approval.

Business support services include free consultations, workshops, and help with loan applications. Local chambers of commerce and business centers provide resources to guide you through the finance process. These services help you prepare strong financial documents and understand credit requirements.

Calculating Costs

Interest rates affect the total cost of equipment finance. Lower rates mean less money paid over time. Rates can be fixed or variable. Fixed rates stay the same, while variable rates can change.

Fees and charges add to the cost. These can include application fees, processing fees, and late payment fees. Always check the list of fees before agreeing.

Using financing calculators helps to estimate monthly payments and total costs. Enter the loan amount, interest rate, and term length. This tool shows how much you will pay each month and overall.

Frequently Asked Questions

What Credit Score Is Needed For Equipment Financing?

A credit score of 600 or higher typically qualifies for equipment financing. Higher scores improve approval chances and rates.

How Hard Is It To Get Equipment Financing?

Getting equipment financing depends on credit score, financial documents, and collateral. Approval can be quick with proper preparation.

How Long Does Equipment Financing Take?

Equipment financing typically takes 1 to 5 business days for approval and fund disbursement. Faster processing depends on credit and documentation.

What Credit Score Is Needed For A $30,000 Loan?

A credit score of 620 or higher typically qualifies for a $30,000 loan. Higher scores improve approval chances. Lenders also consider income and debt.

Conclusion

Getting equipment finance approved takes preparation and clear steps. Check your credit score and gather all financial documents. Understand what lenders want and be ready to show collateral value. Apply early to avoid delays and increase approval chances. Keep communication open with your lender throughout the process.

This helps you stay informed and fix any issues quickly. With good preparation, equipment financing becomes easier and faster. Stay focused and organized to secure the funds you need.