When you apply for credit, your credit profile is under the microscope. But what exactly does a credit profile approval review involve, and why does it matter so much for your financial future?

Understanding this process can give you the power to improve your chances of approval and secure better loan terms. You’ll discover how lenders evaluate your credit profile, what factors influence their decisions, and what you can do to present your strongest financial self.

Keep reading to unlock the secrets behind credit approvals and take control of your financial path.

Credit Profile Basics

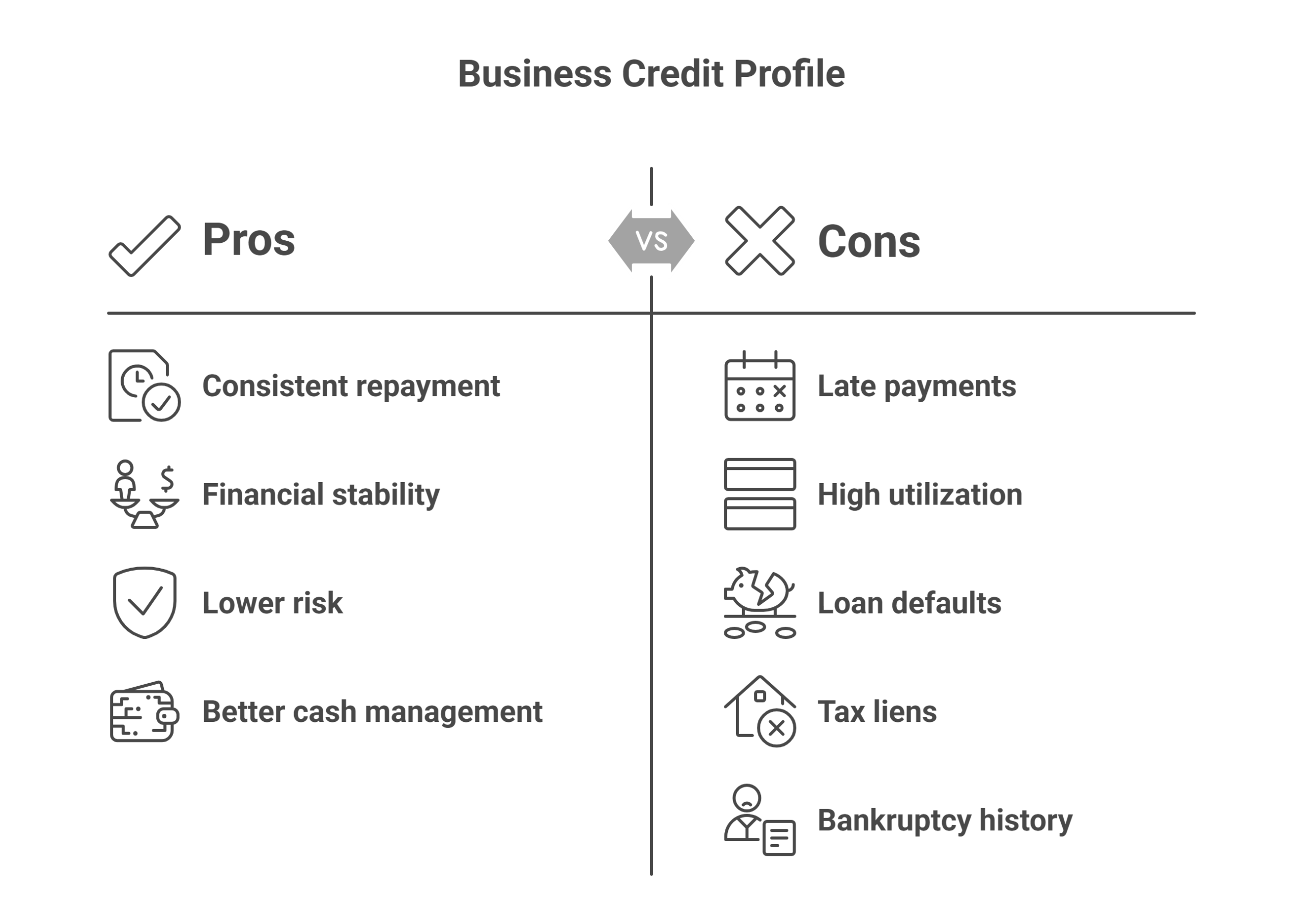

A credit profile includes your credit history, current debts, and payment habits. It helps lenders understand your financial behavior.

Key components are payment history, credit utilization, length of credit, types of credit, and recent inquiries. Each part affects your profile’s strength.

The credit score is a number from your credit profile. It summarizes your creditworthiness in a simple format. The profile shows detailed information behind that score.

A strong credit profile can lead to better loan approval chances. Lenders see you as less risky. A weak profile might cause loan denial or higher interest rates.

Loan approval depends on both your credit score and the full profile. Some lenders look deeper than just the score. They check your overall credit health to decide.

Loan Approval Factors

Debt-to-Income Ratio is a key factor lenders check. It shows how much debt you have compared to your income. A lower ratio means you have more money left to pay new loans. This helps lenders trust you can handle payments.

Credit History and Payment Behavior tell lenders how you managed past debts. Paying bills on time and keeping balances low improves your chances. Missed payments or defaults make lenders cautious.

Income and Employment Verification prove you have a steady source of money. Lenders want to see stable jobs and regular income. This confirms you can pay back the loan reliably.

Fast-tracking Credit Approval

Building a strong credit profile starts with managing your credit well. Pay bills on time to show reliability. Keep credit card balances low to improve your credit utilization ratio. Avoid opening many new accounts at once. This can lower your score and raise concerns.

Improving key credit factors quickly involves focusing on payment history and amounts owed. Set reminders to pay bills before due dates. Consider paying down high balances first. This can help your score rise faster. Checking your credit report often helps spot errors early.

Avoiding common pitfalls means not missing payments or closing old credit accounts unnecessarily. Avoid maxing out credit cards or applying for credit too frequently. These actions can hurt your credit profile and slow approval. Stay consistent and patient for best results.

Credit Review Process

Lenders check several things in a credit review. They look at your payment history to see if you pay bills on time. Your credit score shows how risky it is to lend you money. They also check the amount of debt you have compared to your income. A lower debt to income ratio is better. Lenders want to see a long credit history with responsible use. New accounts or many credit inquiries may lower your chances.

The credit profile evaluation has clear steps. First, lenders collect your credit report from agencies. Then, they analyze key points like credit limits and balances. Next, they assess your ability to repay based on income and debts. Finally, lenders decide if the loan is safe to offer.

Credit reviews help lenders make smart loan decisions. They reduce the risk of lending to someone who may not pay back. This process protects both the lender and the borrower.

Tools And Resources

Monitoring your credit profile is essential for maintaining good financial health. Check your credit reports regularly from the three major bureaus: Experian, TransUnion, and Equifax. Use free online tools or services that offer alerts for any changes or suspicious activities. Keeping an eye on your credit helps spot errors early and prevents identity theft.

Accessing your credit report is free once a year through AnnualCreditReport.com. Review it carefully for mistakes like wrong accounts or incorrect balances. If you find errors, contact the credit bureau to request corrections. Fixing inaccuracies can improve your credit score and increase approval chances.

Professional credit help includes credit counseling and credit repair services. Certified counselors can guide budgeting and debt management. Some services assist in disputing errors and negotiating with creditors. Choose reputable professionals who follow ethical practices and avoid promises of quick fixes.

Regional Insights: Austin, Texas

The local lending environment in Austin is shaped by a mix of banks, credit unions, and online lenders. Many lenders value a well-structured credit profile over just a credit score. Borrowers with steady income and clear financial history often see faster approvals.

Credit approval trends show that timely payments and low debt levels improve chances. Lenders also check for recent credit activity and any negative marks. Profiles with diverse credit types tend to perform better.

Borrowers in Austin can find helpful resources at local credit counseling agencies and financial workshops. Many community groups offer free advice on improving credit health. Online tools and apps also assist in tracking credit status and alerts.

Frequently Asked Questions

What Kind Of Credit Score Do You Need To Buy A $300,000 House?

A credit score of at least 620 is typically needed to buy a $300,000 house. Higher scores improve loan approval chances and rates.

Does Gambling Affect Credit Scores?

Gambling itself does not directly affect credit scores. Overspending or unpaid gambling debts can harm your credit if they lead to missed payments or collections. Lenders focus on payment history, debt levels, and credit usage, not gambling activity. Responsible financial management maintains a healthy credit score.

How Rare Is An 830 Fico Score?

An 830 FICO score is extremely rare, placing you in the top 1% of consumers. It reflects excellent credit management and low risk.

Which Credit Score Does Truist Use?

Truist primarily uses the FICO Score 8 model from Experian for credit decisions. They may also consider other scores and credit factors.

Conclusion

A strong credit profile plays a big role in approval decisions. Lenders check your credit history to see if you repay loans on time. Keeping accounts current and managing debt well improves your profile. Regularly reviewing your credit helps spot errors and areas to improve.

Understanding how lenders assess your credit can guide better financial choices. Stay consistent and patient to build trust with lenders. Good credit habits open doors for future borrowing needs.