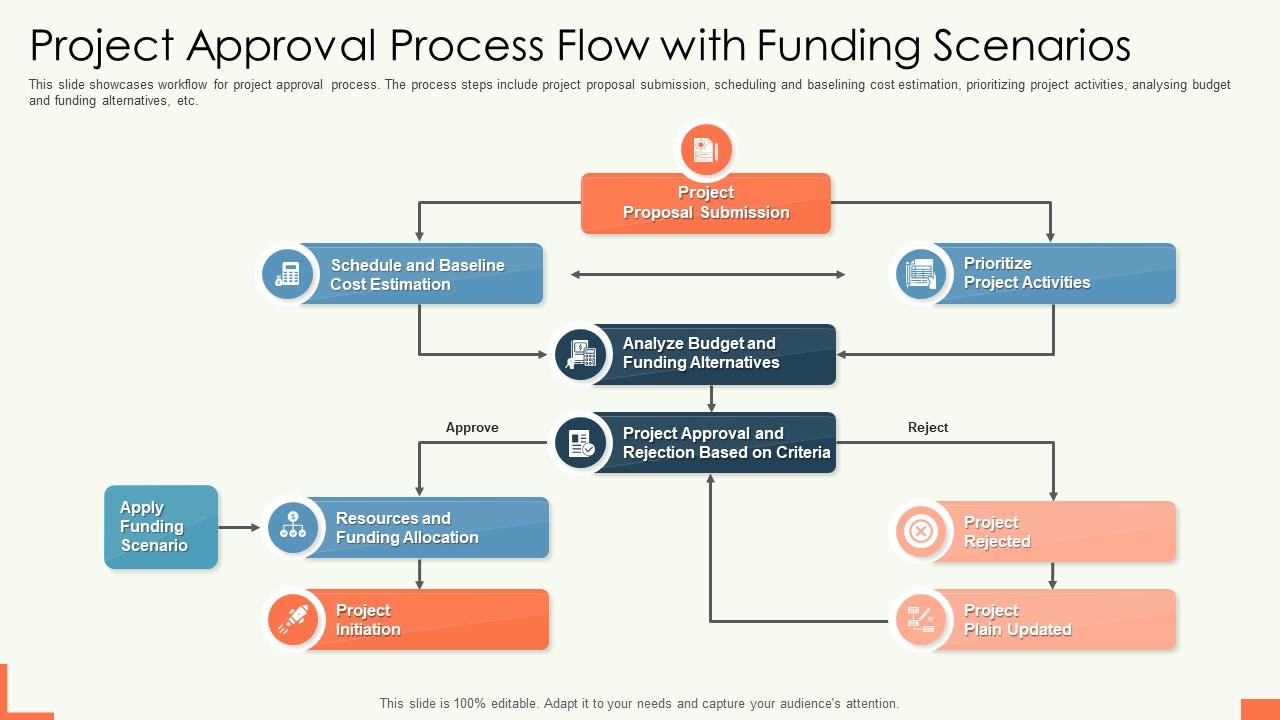

If you’re looking to grow your business, understanding the business funding approval process is key to getting the money you need, when you need it. Knowing what lenders look for and how they decide to approve your application can make a huge difference in your success.

You might wonder what steps you need to take, what documents to prepare, or how long the process really takes. This guide breaks down everything in simple terms, helping you avoid common pitfalls and boost your chances of approval. Keep reading to discover how you can navigate the process with confidence and secure the funding that drives your business forward.

Types Of Business Funding

Traditional bank loans require good credit and a strong business plan. Banks often want to see steady revenue and a clear repayment plan. The approval process can take weeks, and the paperwork is usually extensive. Interest rates tend to be lower than other options, but qualification rules are strict.

SBA loans are backed by the U.S. government. This makes them less risky for lenders and easier to get than traditional loans. They offer long repayment terms and lower down payments. The process includes application, underwriting, and approval, which can take a few weeks to months.

Online lenders provide faster access to funds. They use technology to speed up approvals, often within days. Credit requirements are more flexible, but interest rates may be higher. Online loans suit businesses needing quick cash for short-term needs.

Alternative funding options include invoice financing, merchant cash advances, and crowdfunding. These options have varied terms and costs. They are useful for businesses with unusual needs or weaker credit. Approval is usually faster but can be more expensive.

Loan Application Essentials

Gathering the required documents is the first step in a loan application. Personal and business credit scores show lenders your creditworthiness. A higher score means better chances of approval.

Financial statements include income, expenses, and cash flow details. These prove your business’s ability to repay the loan. Lenders review balance sheets and profit-loss statements closely.

Your business plan and projections explain how you will use the funds. Clear plans and realistic forecasts show lenders you have a solid strategy. This builds trust and confidence in your business.

Pre-qualification Steps

Assessing creditworthiness is the first step in business funding approval. Lenders check your personal and business credit scores to see if you pay debts on time. A higher score means better chances of approval.

Next, business age and industry are important. Older businesses with a stable track record often get preferred. Some industries are riskier, so lenders look closely at those.

Revenue and cash flow show if the business can pay back the loan. Lenders want to see steady income and positive cash flow. This proves the business is healthy and can handle loan payments.

Underwriting Process

Risk analysis checks the chance of loan default. Lenders study business history, cash flow, and market conditions. They want to be sure the loan is safe.

Verification of information means lenders confirm all details in your application. This includes income, credit scores, and legal documents. Accuracy is key to avoid delays or rejection.

Collateral assessment looks at assets offered to secure the loan. Common collateral includes property, equipment, or inventory. The value must cover the loan amount to reduce lender risk.

Approval And Funding

Loan Decision Factors include credit score, business history, and cash flow. Lenders also check industry risks and repayment ability. A strong personal and business credit score improves approval chances.

Loan Agreement and Signing happens after approval. The agreement lists loan terms, interest rates, and repayment schedules. Borrowers must read carefully before signing. Signing confirms the borrower accepts the loan conditions.

Disbursement of Funds is the final step. Funds are sent to the borrower’s account. This usually happens within a few days after signing. Proper use of funds is important to avoid default.

Tips For Fast Approval

Improving your credit score helps lenders trust your ability to repay. Pay bills on time and reduce debt. Check your credit report for errors and fix them quickly. A higher score often means faster approval and better terms.

Organizing documentation saves time during the application process. Gather financial statements, tax returns, and business plans early. Keep everything clear and easy to find. This shows lenders you are prepared and serious.

Choosing the right lender can affect approval speed. Some lenders specialize in certain industries or loan types. Research and select one that fits your business needs. Compare interest rates, fees, and requirements before applying.

Common Approval Challenges

Insufficient revenue can cause lenders to doubt your ability to repay loans. Small or new businesses often face this challenge. Showing steady income helps build lender confidence.

Poor credit history lowers approval chances. Lenders check credit scores and past debts. A history of missed payments or defaults signals risk. Improving credit before applying is wise.

Incomplete applications slow down or block approval. Missing documents or unclear info cause delays. Double-check all forms and include requested paperwork. A complete application shows professionalism and readiness.

Using Funds Wisely

Budgeting for growth means planning how to spend funds to expand your business. Start by listing all costs needed for growth, such as new equipment, hiring, or marketing. Keep track of expenses to avoid overspending.

Repayment planning is key to avoid financial trouble. Know your loan terms and set aside money each month to pay back on time. Missing payments can hurt your credit and business reputation.

Maintaining financial health means watching your cash flow closely. Keep records of income and expenses. Save some money for emergencies. Regularly check your financial status to make smart decisions and keep your business stable.

Frequently Asked Questions

How Long Does It Take To Get Approved For Business Funding?

Business funding approval typically takes 1 to 5 business days, depending on the lender and application completeness. Some loans may take longer.

What Is The Monthly Payment On A $50,000 Business Loan?

The monthly payment on a $50,000 business loan depends on the interest rate and loan term. For example, at 7% interest over five years, payments are about $990. Use a loan calculator for precise amounts based on your specific terms.

What Credit Score Do You Need To Get A $30,000 Loan?

A credit score of at least 620 typically qualifies you for a $30,000 loan. Higher scores improve approval chances and rates.

What Credit Score Do You Need For Business Funding?

Lenders typically require a personal credit score of 600 or higher for business funding approval. Higher scores improve loan chances. Some loans may accept lower scores but often involve higher interest rates or stricter terms. Maintaining strong business financials also boosts funding approval odds.

Conclusion

Securing business funding takes clear steps and careful planning. Prepare your documents and know what lenders want. Strong credit and steady revenue improve your chances. Stay patient through reviews and underwriting checks. Understanding the process helps you move forward confidently.

Keep your goals in mind and remain organized. This approach increases your chances of getting approved. Funding your business is possible with the right effort.