Are you in the middle of buying a home and just heard about conditional mortgage approval? It can feel confusing and a bit stressful.

But understanding the exact steps involved can give you the confidence you need to move forward. Conditional mortgage approval means your lender has reviewed much of your financial information but needs a few more things from you before giving the final green light.

Knowing what these steps are and how to handle them can help you avoid surprises and speed up your loan process. You’ll get a clear, simple breakdown of each step you’ll face after conditional approval—so you can stay in control and get closer to owning your dream home.

Conditional Approval Basics

Conditional approval means the lender reviewed your file but needs more information. It is not a final yes yet.

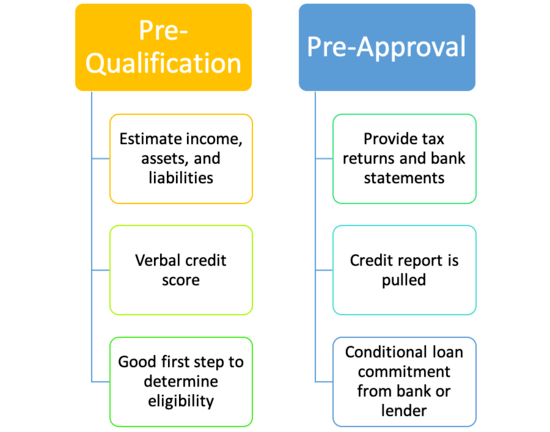

This is different from preapproval, which is an early estimate based on basic info. Final approval means all checks are done.

| Type of Approval | Description |

|---|---|

| Preapproval | Based on initial info; not guaranteed |

| Conditional Approval | Underwriter reviewed file; needs more documents or actions |

| Final Approval | All conditions met; loan ready to fund |

Common conditions include proof of income, updated bank statements, or resolving credit issues. These must be met to get the loan fully approved.

Steps To Receive Conditional Approval

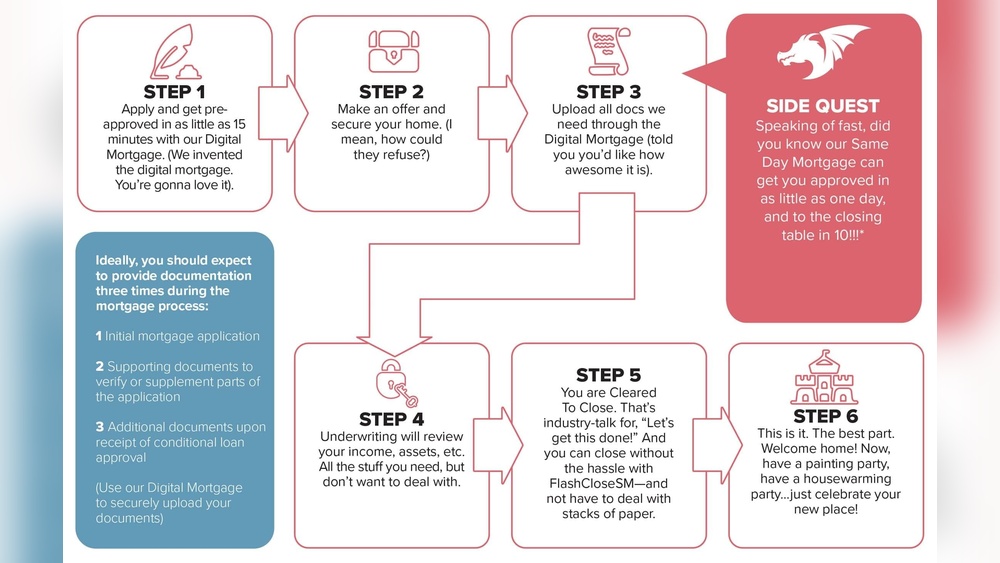

Submitting your mortgage application starts the process. Lenders need complete and accurate information. This includes personal details, income proof, and credit history. Missing documents can delay approval.

The initial documentation review checks all papers for correctness. Lenders verify your identity, income, and employment status. They also review your credit report for any issues.

During underwriting assessment, an expert evaluates your financial health. This step measures your ability to repay the loan. The underwriter may ask for more documents or explanations.

Conditional approval means the underwriter tentatively agrees to the loan. You must meet specific conditions like providing extra paperwork or clearing debts. Once these are met, final approval follows.

Typical Conditions To Meet

Income and employment verification confirms your job status and earnings. Lenders need recent pay stubs, tax returns, or employment letters. This step proves you can repay the loan.

Asset and bank statement requirements show your savings and funds. Lenders want to see enough money for down payment and closing costs. Recent bank statements and proof of assets are needed.

Credit report and score checks reveal your credit history. Lenders assess your debt and payment habits. A good credit score helps secure better loan terms.

Property appraisal and title clearance ensure the home’s value matches the loan. An appraiser checks the property’s condition and market price. Title clearance confirms no legal claims exist on the property.

Handling Conditional Approval

Gathering additional documents is key after conditional approval. Lenders ask for proof like pay stubs, bank statements, or tax returns. Submit these quickly to avoid delays. Keep copies of all papers for your records.

Communicating with your lender helps keep the process smooth. Ask questions if you don’t understand something. Respond to emails or calls promptly. Good communication shows you are serious and organized.

| Timeline | What to Do | Why It Matters |

|---|---|---|

| Within 3 days | Submit requested documents | Prevents delays in loan approval |

| Within 7 days | Check for lender updates | Stay informed about your loan status |

| Before deadline | Meet all conditions set by lender | Ensures final approval of your loan |

Challenges And Risks

Common reasons for denial after conditional approval include changes in income, new debts, or missing documents. Lenders want to see stable finances and complete paperwork.

Delays and denials often happen when borrowers do not respond quickly to lender requests. Keeping all documents ready speeds up the process. Avoid making large purchases or applying for new credit during this time.

Financial changes during the process can cause trouble. A job loss, reduced hours, or increased debt might lead to denial. Staying financially steady until final approval is key to success.

| Challenge | How to Avoid |

|---|---|

| Missing Documents | Submit all required papers promptly |

| Income Changes | Keep your employment and income stable |

| New Debt | Avoid new loans or credit cards |

| Delayed Responses | Reply quickly to lender requests |

Tips For Final Mortgage Approval

Keep your finances stable by avoiding new debts or large purchases. Saving money is important to meet lender conditions. Pay bills on time and do not close bank accounts. This shows your lender you are responsible with money.

Respond quickly to all requests from your lender. They may ask for extra documents or information. Fast replies help keep the mortgage process moving smoothly. Delay can cause problems or slow down approval.

Work well with your mortgage team. Stay in touch with your loan officer, real estate agent, and underwriter. Ask questions if you do not understand something. Clear communication helps avoid mistakes and surprises.

What Happens After Conditional Approval

The final underwriting review checks all your documents again. This step confirms your income, assets, and credit information. The underwriter makes sure all conditions are met before full approval.

Preparing for closing means gathering all needed paperwork. You will receive a closing disclosure that shows loan terms and costs. Review it carefully and ask questions if something is unclear.

Ensuring smooth loan funding involves coordinating with your lender and the title company. Funds are sent to the seller after closing. This step completes the home buying process.

Frequently Asked Questions

How Long Does A Conditional Approval Take For A Mortgage?

A conditional mortgage approval typically takes 1 to 3 days after underwriting reviews your documents. Meeting lender conditions speeds final approval.

How Likely Is It To Get Denied After Conditional Approval?

Denial after conditional approval is rare but possible if conditions are unmet or financial situations worsen. Stay organized and responsive.

Is It Good If The Underwriter Gives Conditional Approval?

Conditional approval shows the underwriter supports your loan, pending you meet specific conditions. It’s a positive and common step toward full approval.

What Happens If You Are Conditionally Approved For A Mortgage?

Conditional mortgage approval means the lender will fully approve your loan once you meet specific requirements. Complete requested documents promptly. The lender verifies your income, assets, and credit details. This step is normal and not a final approval. Meeting conditions leads to loan finalization and closing.

Conclusion

Conditional mortgage approval marks a key step in home buying. It means the lender reviewed your documents and set conditions. Meeting these conditions moves you closer to full approval. Stay organized and submit requested information quickly. This helps avoid delays or denial.

Understanding these steps reduces stress and boosts confidence. Keep focused on fulfilling lender requirements. Soon, you’ll reach final mortgage approval and own your home.